Key Points

- The federal funds rate is set by the U.S. Federal Reserve and affects overnight bank lending.

- LIBOR is a global benchmark rate set by major banks in London for short-term loans.

- The federal funds rate and LIBOR are affected by geography, with the former in the U.S. and the latter in London.

- LIBOR is transitioning to other benchmarks like the Secured Overnight Financing Rate (SOFR).

- The prime rate is closely tied to the federal funds rate, influencing consumer loan costs.

Federal Funds Rate vs LIBOR: An Overview

In macroeconomics, the interest rate plays a vital role in delivering an equilibrium in the asset market by equating the demand and supply of funds. Two of the most prominent interest rates widely featured are the federal funds rate and the London Interbank Offered Rate (LIbor). These rates impact a range of financial products, from mortgages to corporate loans.

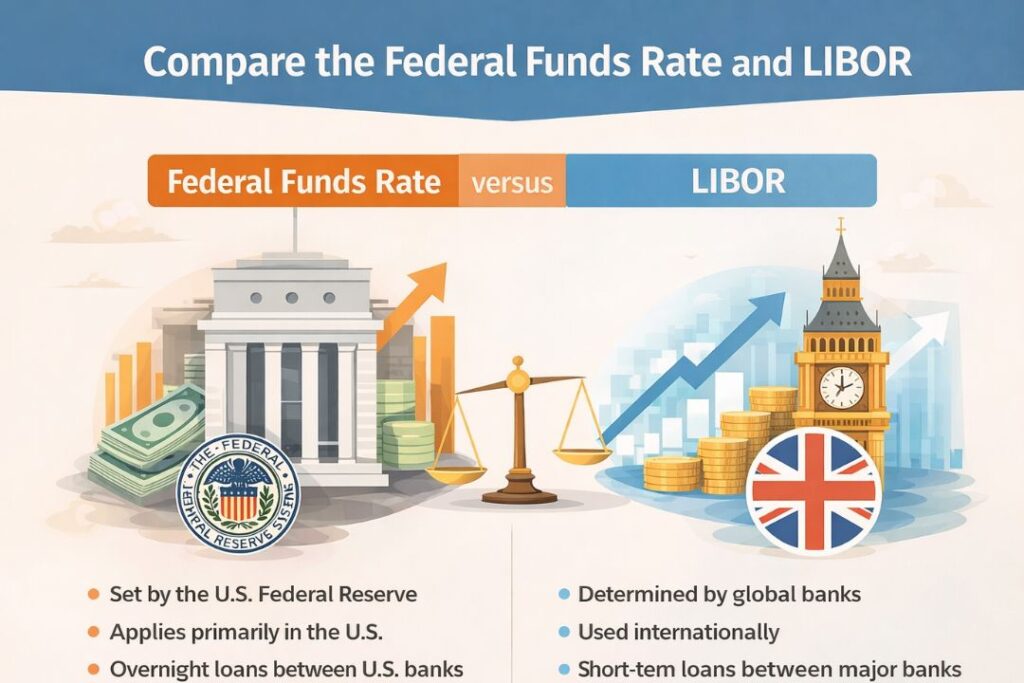

The federal funds rate is mostly pertinent for the U.S. economy, as it represents the interest rate for highly creditworthy U.S. financial institutions’ trading balances held at the Federal Reserve, usually overnight. The U.S. The Fed sets the federal funds rate.

LIbor represents a benchmark rate that leading global banks charge each other for short-term loans. Unlike the federal funds rate vs LIBOR is determined by the balance between supply and demand on the funds market, and it is calculated for five currencies and different periods ranging from one day to one year.

Keep reading to learn more about the federal funds rate vs LIBOR.

Understanding the Federal Funds Rate

The federal funds rate is one of the most important interest rates for the U.S. economy, as it affects broader economic conditions in the country, including inflation, growth, and employment. The Federal Open Market Committee (FOMC) sets the target for the federal funds rate and achieves the predetermined rate through open market operations.

The federal funds rate is set in the US. and is typically charged on overnight loans. The fed funds rate is the interest rate at which commercial banks lend reserves to each other on an overnight basis

A Closer Look at LIBOR

LIBOR is an important rate used globally by financial institutions to determine the interest rate to be charged on various loans. However, the transition away from LIBOR to other benchmarks, such as the Secured Overnight Finance Rate (SOFR), began in 2020.

LIBOR is based on five currencies: Dollar, Euro, Pound Sterling, Japanese Yen, and Swiss Franc. There are typically seven maturities for which LIBOR is cited: overnight, one week, and one, two, three, six, and 12 months. The most popular LIBOR rate is a three-month rate based on the U.S. LIBOR rate. dollars.

Compared the Federal Funds Rate and LIBOR

Many differences exist between LIBOR and the fed funds rate. First is geography—the federal funds rate is set in the U.S., while LIBOR in London. That doesn’t mean that loans or other loans issued in the United States do not use LIBOR as their benchmark. In fact, many loans do. For example, some mortgage rates are set to “prime”or LIBOR plus some markup.

The fed funds rate, while given as a target by the Federal Reserve, is actually achieved in the market for overnight borrowing among financial institutions. The Fed does established a fixed rate, known as the discount rate, which is the interest rate that the Fed will lend to banks through the so-called discount window.

The discount rate is always set higher than the federal funds rate target, and so banks would prefer to borrow from another rather than pay higher interest to the Fed. However, if the demand for reserves is adequate, then the fed funds rate will tick up. LIBOR, on the other hand, is set by a consortium of investment houses in London each day without a market mechanism.

While most small and mid-sized banks borrow federal funds to meet their reserve requirements—or loan their excess cash the central bank isn’t the only place they can go for competitively priced short-term loans. They can also trade eurodollars, which are US-dollar denominated deposits at foreign banks. Because of the size of their transactions, many larger banks are willing to go offshore if it means a slightly better rate.

For a long time, LIBOR was presumably the most influential benchmark rate in the world. The Intercontinental Exchange (ICE) group asks several large banks how much it would cost them to borrow from another lending institution each day. The filtered average of the responses represents LIbor. Eurodollars come in various periods, so there are actually multiple benchmark rates—one-month LIBOR, three-month LIBOR, and so on.

Because eurodollars are a substitute for federal funds, LIBOR tends to track the Fed’s key interest rate rather closely. However, unlike the prime rate, there were significant deviations between the two during the financial crisis of 2007–2009.

How the Federal Funds Rate vs LIBOR Effect the Prime Rate

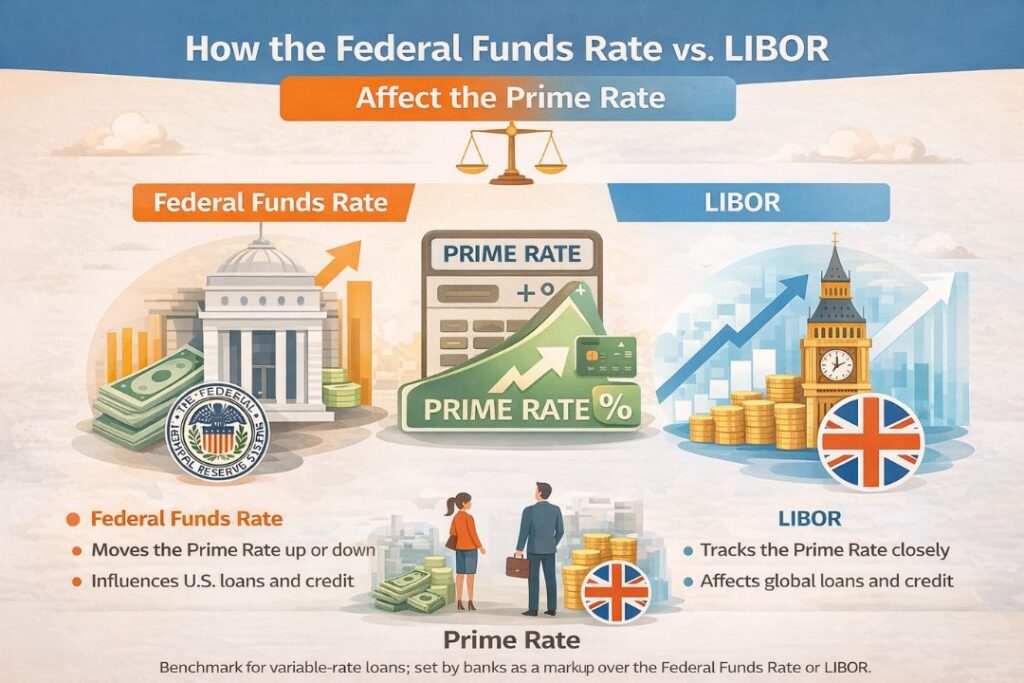

Whereas most variable-rate bank loans aren’t directly tied to the federal funds rate, they usually move in the same direction. That’s because the prime and LIBOR rate, two important benchmark rates to which these loans are frequently pegged, have a close relationship with the federal funds rate.

In the case of the prime rate, the link is especially close. Prime is usually considered the rate that a commercial bank offers to its least-risky clients. The Wall Street Journal asks 10 major banks in the US what they charge their most creditworthy corporate clients. It publishes the average on a daily basis, albeit it only changes the rate when 70% of the respondents adjust their rate.

Whereas each bank sets its own prime rate, the average hovers above the federal funds rate. Consequently, the two figures move in virtual lock-step with each other.

If you’re an individual with average credit, your credit card may charge premium plus, say, six percentage points. If the federal funds rate is at 1.5%, that means prime maybe at 4.5%. So, consumers would be paying 10.5% on their revolving credit lines. If the Federal Open Market Committee lowers the rate, they will experience lower borrowing costs almost immediately.

Conclusion

- Summary of Key Differences: Highlight the main differences between the federal funds rate vs LIBOR, such as their geographical importance, how they are set, and their influence on the economy.

- Interest Rate Influences: Explain how both rates influence other interest rates like corporate bonds, mortgages, and loans.

- Current Transition: Mention the shift from LIBOR to alternative benchmarks like the Secured Overnight Finance Rate (SOFR) and its implications.

- Practical Impact: Discuss how changes in these rates impact consumers and businesses, especially regarding borrowing costs.

(Old Key Takeaways, if they help) Benchmark interest rates are essential for setting interest rates on all kinds of debts, from corporate bonds to mortgages to the rate that banks lend to each other.

The federal funds rate is established by a market mechanism for overnight borrowing on reserves, and a target is set by the FOMC.

LIBOR has several maturities, with the interest rate set in London through a consortium of financial institutions.

FAQs

1. What is the federal funds rate?

The federal funds rate is the interest rate set by the U.S. Federal Reserve at which banks lend money to each other overnight.

2. What is LIBOR?

LIBOR (London Interbank Offered Rate) is a benchmark interest rate used globally for short-term loans between banks.

3. How are the federal funds rate and LIBOR different?

The federal funds rate is controlled by the U.S. Federal Reserve, while LIBOR is based on estimates from major banks in London.

4. Why is LIBOR being replaced?

LIBOR is being phased out due to concerns about reliability and transparency, and it is being replaced by rates like SOFR.

5. How do these interest rates affect consumers?

These rates influence borrowing costs such as mortgages, credit cards, and other loans.

Disclaimer : The information provided in this article is for educational and informational purposes only and should not be considered financial or investment advice. Readers should conduct their own research or consult a qualified financial advisor before making any financial decisions.