Key Points

- Set clear financial objectives to guide spending and build wealth.

- Include budgeting, saving, and managing debt in your financial plan.

- Use automatic transfers to streamline achieving financial goals.

- Regularly review and adjust your financial objectives as needed.

- Follow the 50/30/20 rule for effective budgeting.

Setting financial goals is an essential step to securing long-term sustainability for you and your family. You’ll need to prioritize goals and set milestones for achieving short,middle and long-term goals. Here’s a step-by-step guide to set financial goals that align with your needs and aspirations.

Without clear goals, it’s easy to overspend, under-save, or miss out on key financial opportunities. Whether you are looking to build wealth, retire comfortably, or eliminate debt, having a structured financial plan will help you stay on track and make informed decisions.

“You have to plan early and figure out what’s most important to you—maybe it’s figuring out a budget or sending your kids to college,” says Noah Damsky, founder of Los Angeles-based Marina Wealth Advisors. “The sooner you get clear on these priorities, the earlier you can actually start planning for where you want to go—and the more likely it is that you’ll succeed.”

Understanding Various Types of Financial Goals

Financial objectives typically fall into three categories: short-term, mid-term, and long-term. They each require differing levels of commitment, but they’re all important components of your overall long-term financial plan. By understanding the differences, you can allocate your resources effectively and improve your chances of achieving financial success.

Short-Term Goals

Short-term financial goals can usually be accomplished within a year. They generally concentrate on financial stability and building a solid foundation. Examples include:

- Creating a monthly budget

- Building an emergency fund

- Payment off high-interest credit card debt

- Setup automatic savings contributions

By tackling short-term goals, you can create a financial cushion that prevents unnecessary stress when unexpected expenses arise—allowing you to work on long-term goals more easily.

Mid-Term Goals

Medium-term goals usually take three to five years and require strategic planning. Normally, these goals involve substantial financial resources—such as saving up for a big purchase or paying down large amounts of debt. Examples include:

- Paying off student loans

- Save for a down payment on a home

- Buying a vehicle with minimal or no financing

- Investing in higher education and professional development

Mid-term goals bridge the gap between immediate financial sustainability and long-term wealth creation. To achieve them, you’ll need to navigate some uncertainty and make adjustments to overcome barriers.

Long-Term Goals

Long-term goals take longer than five years and often include securing your financial independence and prosperity. Examples include:

- Planning for retirement

- Paying off a mortgage

- Creating generational wealth

- Establishing an estate plan

“Time is your biggest advantage when it comes to long-term financial planning,” says Damsky. “The earlier you start saving for retirement, the less financial stress you’ll face later.”

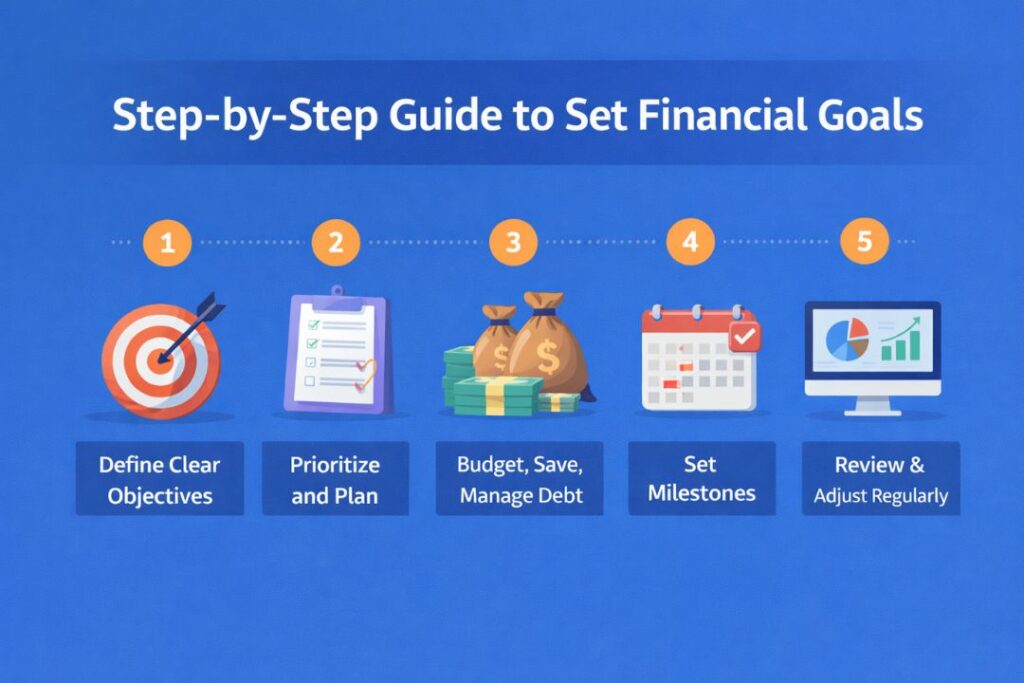

Step-by-Step Guide to Set Financial Goals

A structured approach to goal-setting can ensure you remain on track and make steady progress. It may appear intimidating to take stock of your financial situation and develop a plan to accomplish your goals, but following these easy steps can help you strike the right balance between realistic and rewarding goals.

Assessment

Before setting goals, take a close look at your financial position. Evaluate your income, expenditures, savings, and debt to get a clear picture of how much money you’re bringing in, how much you’re spending, and what you’re spending it on. A thorough assessment will help you set realistic, attainable goals and create a financial plan that aligns with your lifestyle and future aspirations.

Define Your Financial Goals

Think about what you want to achieve. If you’re fresh out of college and just starting a full-time job, you may prioritize creating an emergency fund or paying off your student loans. If you’re a new parent, you may want to begin a college fund for your child.

Whatever your goals are, make sure to think about how you’ll actual reach them. Using the SMART goals framework—setting specific, measurable, achievable, relevant, and time-bound goals—can help ensure your objectives are attainable while holding you accountable.

For example, don’t just say “I want to save more money.” Instead, you should set a specific goal, such as “I will save $30,000 for a down payment on a house in five years by setting aside $500 per month.”

Prioritize Your Goals

Some financial objectives are more important than others. For example, building an emergency fund should come before investing in stocks to avoid taking on debt to pay for unpredictable expenses.

Similarly, you should consider paying down debt with a high interest rate, especially if your monthly credit card payments become excessively cumbersome. Ranked your goals based on urgency and long-term impact and determine which ones to tackle first.

crafting an effective financial plan

A financial plan helps you manage income, expenses, and savings while staying focused on long-term goals. It covers several key components, such as budgeting, debt management, and savings.

Budgeting

A strong budget is the foundation of any financial plan—and gratefully, developing one can be simple.

“There’s a stigma to budgeting where people think it’s boring and you need to list out every single dollar on a spreadsheet, but it really doesn’t have to be that difficult,” says Daniel Milks, the founder of South Carolina-based Woodmark Wealth Management. “There are so many tools online where you can link your bank account or credit card, and they’ll show you rough how you’re spending your money.”

Budgeting apps to consider include Mint and YNAB, but they’re not for everybody. If you prefer, you can use a budgetary calculator instead.

Many people find it simpler to budget when they follow a specific strategy. One popular method is the 50/30/20 rule—allocated 50% of income to needs, 30% to wants, and 20% to savings—but some financial advisors suggest a different approach. “One of the most effective strategies is to pay yourself first,” says Milks. “Before covering any other expenses, set aside money for savings and investments to ensure your future financial security.”

50/30/20 Rule

The 50/30/20 rule provides an easy rule of thumb for your monthly budget: 50% of your income should go towards necessary expenses, 30% on wants, and 20% on savings.

Building an Emergency Fund

An emergency fund provides much-needed financial security when the unpredictable happens, like losing a job or a medical emergency. Experts recommend saving three to six months’ worth of essential expenses, but Damsky advises that “self-employed individuals or those with irregular income should aim for closer to 12 months of savings.” After determining how much you should save, calculate how much you can save each month and how long it will take to grow your emergency fund. Then, begin putting money into an easily accessible savings account.

Debt Management

Smart debt management is key to achieving financial health, and there are many different strategies you can utilize. The avalanche method prioritizes high-interest debts first in order to minimize long-term costs, while the snowball method focuses on paying off smaller debts first to build momentum.

That said,not all debt is bad. “For example, a low-interest mortgage can be a financial tool because it frees up money for smart high-yield investments, while high-interest debt like credit cards should probably be aggressively paid off,” says Damsky.

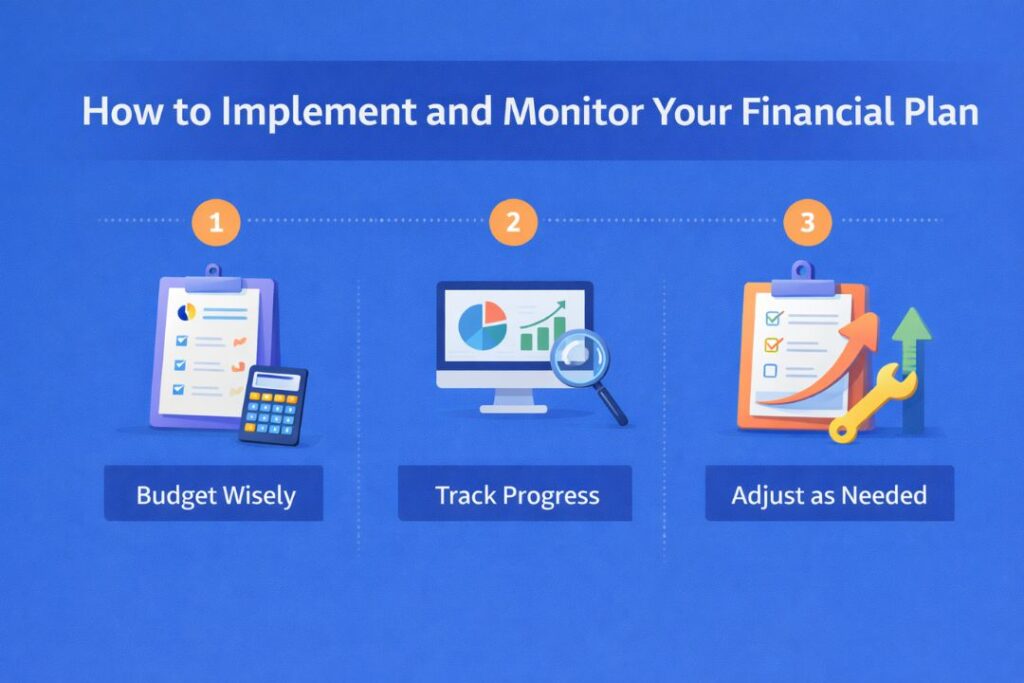

How to Implement and Monitor Your Financial Plan

Once your financial plan is in place, take steps to make achieving your goals easier. You should also consistently monitor and adjust it to align with your developing financial situation (a new job, for example) and goals.

Automate Savings and Investments

Setting up automatic transfers to savings and investment accounts can help you stick to your goals and stop the temptation to spend. Contribute routinely to a 401(k), Roth IRA, or high-yield savings account until you make it a habit, which increases your chance of staying on track with your financial goals.

Regularly review and adjust your goals

Financial situations evolve, so reviewing and adjusting your goals is essential. “Your financial goals aren’t set in stone,” says Milks. “Life changes—like marriage, having children, or switching careers—can impact your financial priorities.” At the very least, you should be reviewing your plan—and adjusting it as necessary—once a year.

Overcoming Common Challenges in Finance

Even the best financial plans encounter setbacks, but you can take steps to ensure your plan is as foolishproof as possible. Here’s how to address common setbacks with goal-setting:

- Underestimating Expenses: Track spending carefully to avoid financial shortcomings.

- Procrastination: Set calendar reminders for financial check-ins and assign someone to help hold you accountable.

- Emotional Spending: Establishment spending limits to avoid impulse purchases.

- Ignoring Tax Implications: Consult with a financial advisor to maximize tax-efficiency savings and investments.

Conclusion

Financial goal setting is an ongoing process that requires planning, discipline, and flexibility. Understand your situation and set clear preferences to develop goals that align with the future you want for yourself and your family. By maintaining a strong budget, building an emergency fund, and making informed investment choices, you can work toward more ambitious goals like a healthy retirement or putting your children through college.

“The most important step is to begin,” says Damsky. “You can always refine your goals, but having a plan and keeping it in motion is what really matters.”

FAQ

What are financial objectives and why are they important?

Financial goals are goals you set for how you want to manage, save, and use your money. They help you remain focused, avoid unnecessary spending, and build long-term financial stability.

What is the difference between short-term, medium-term, and long-term financial objectives?

Short-term goals usually take less than a year, such as creating an emergency fund. Medium-term goals take around three to five years, like savings for a car or paying off debt. Long-term goals take many years and include things like retirement planning or purchasing a house.

How can I start setting realistic financial objectives?

Begin by reviewing your income, expenses, and savings. Then decide what you want to accomplish financially and set clear timelines for each goal. Breaking big goals into smaller steps makes them easier to accomplish.

What is the 50/30/20 budgeting rule?

50/30/20 rule It suggests spending 50% of your income on needs, 30% on desires, and saving 20% for future goals or investments.

How often should I review my financial objectives?

It is a good idea to review your financial goals at least once or twice a year. This helps you adjust your plan if your income, expenses, or preferences change.

Disclaimer :The information provided in this article is for educational and informational purposes only and should not be considered financial or investing advice. Financial circumstances vary from person to person, and readers should conduct their own research or consult a qualified financial advisor before making any financial decisions. The author and this website are not liable for any losses or damages that may occur from the use of the information provided in this content.