Introduction

Every parent dreams of giving their children the best education, financial security, and a strong foundation for the future. However, with rising education costs, inflation, and unpredictable life events, planning for your child’s financial future has become more important than ever. Choosing one of the Best Child Insurance Plans in India can help parents build a dedicated financial corpus while ensuring life cover protection in case of unforeseen circumstances.

A Child Insurance Plan is designed to help parents systematically build a financial corpus for their child’s future goals such as higher education, marriage, or starting a business while also providing life insurance protection. Today, the Best Child Insurance Plans in India combine investment growth, guaranteed returns, and premium waiver benefits to ensure that even if something unfortunate happens to the parent, the child’s future dreams remain protected and financially stable.

What is a Child Insurance Scheme? A Complete Guide to the Best Child Insurance Plans in India

A child insurance plan is a financial product designed to help parents build a dedicated savings corpus for their child’s future needs, including higher education, marriage, or starting a business, while also offering life insurance protection. The Best Child Insurance Plans in India combine disciplined investment growth with financial security, ensuring that the child’s goals remain protected even in unsure circumstances. Most child insurance plans include two essential elements:

- Savings/investment guaranteed benefits (endowment/participating) or market linked growth (ULIP/market-linked savings).

- Protection life cover that ensures the policy continues or pays a lump sum if the assured (often the parent/proposer) dies during the policy term. This protects the child from losing planned funds if the bread winner dies prematurely.

Different products emphasize different balances of security (guaranteed returns) vs growth potential (market linked/ULIP).

Why Consider the Best Child Insurance Plans in India – And When Not To?

Reasons for families to buy child plans

- Forced savings: An insurance policy with scheduled premiums helps disciplined savings.

- Protection: many plans waive future premiums on the death/critical sickness of the parent so the child still receives the corpus.

- Milestone payouts: Payments timed to education/marriage milestones give structured funding.

- Tax benefits: Premiums and maturity proceeds often enjoy tax benefits under Indian tax law (see section 7).

When You May Not Prefer the Best Child Insurance Plans in India

- Cost/value: some child plans (especially ULIPs with higher charges) may underperform a combination of a term insurance + mutual fund SIPs. If your priority is maximizing returns, a term + SIP approach often beats conventional child plans net of charges.

- Liquidity : Child plans are long term; surrendering within early years can lead to low returns or penalties.

- Transparency: check the fund/charge structure—some ULIPs and participating endowments carry costs that dent returns.

In short, the Best Child Insurance Plans in India are ideal for parents who prioritize safety, protection, and structured payouts for their child’s future. However, if your main goal is higher growth with lower costs, a combination of term insurance and systematic investments may be a better option.

Main types of child insurance plans pros & cons

Traditional Endowment/Participating child plans

- How they work: guaranteed sum insured + bonuses/participating additions.

- Pros: predictable, guaranteed minimum payouts, lower risk.

- Cons: Modest returns compared to equity products; Bonuses depend on the insurer’s performance.

ULIPs (Unit Linked Insurance Plans) (e.g., market-linked child ULIPs)

- How: Premium is divided into life cover + units invested in funds (equity, debt, balanced).

- Pros: higher downside potential, switching between funds, partial withdrawals after lock-in.

- Cons: Fund management charges, premium allocation charges, mortality and fund risks. Performance depends on the market.

Guaranteed return child plans

- How: Structured guaranteed payouts at future dates. occasionally called guaranteed endowments.

- Pros: uncertainty, easy planning.

- Cons : Lower returns, product terms must be read carefully.

Term + Separate investments

- How: Buy a large term life policy (pure protection) and invest the difference into mutual funds (SIP) or PPF for the child.

- Pros: best cost-to-coverage ratio, higher expected returns through equity SIP.

- Cons : requires active discipline and rebalancing parents must be certain they’ll continue investments.

What to Look for in the Best Child Insurance Plans in India – 12-Point Checklist

Before buying, evaluate every plan against these important points:

Who is covered?: parent, child, or both. Many plans are taken on parents’ life; some cover the child.

Premium waiver on death: does the insurer waive future premiums on the insured’s death? Are there a waiting/claim process?

Payout schedule: single maturity versus staged payouts for education milestones. Timings should match your anticipated needs (e.g., college at 18).

Guaranteed additions & bonuses: participating plans may add reversionary/Terminal bonuses. How are these declared?

Investment options & fund choices (for ULIPs): number of funds, equity/debt mix, switching flexibility, auto-rebalance features.

Charges & transparency: look for premium allocation charges, fund management charges, policy administration charges, mortality charges.

Lock-in and partial withdrawal rules: ULIPs have a 5-year lock-in; some plans permit partial withdrawals after a certain period.

Surrender value & exit penalties: yields can collapse if you surrender in early years.

Loan facility: is policy loan available (useful for emergencies)? Terms and limits?

Riders/add-ons: critical illness rider, accidental death benefit, waiver of premium for other events.

Claim settlement record & service: insurer reputation, claim settlement ratio, customer service reviews.

Tax treatment: premium tax deductions, taxableness of maturity — check Sec 80C/10(10D) details.

If a plan scores well on the first five and is transparent on charges, it’s usually worth consideration.

Detailed profiles top plans & providers (features, pros & cons)

Market context: India’s insurance sector witnessed regulatory and market changes recently (e.g., FDI cap changes and new product launches). These shifts impact product design and competition, so always confirm current product brochures before purchase.

Below are concise but deep profiles of the noteworthy providers and their popular child plans. Each insurer is given a short profile with plan highlights, typical use cases, benefits, and pitfalls to watch for. Sources used are the insurer’s product pages and official brochures.

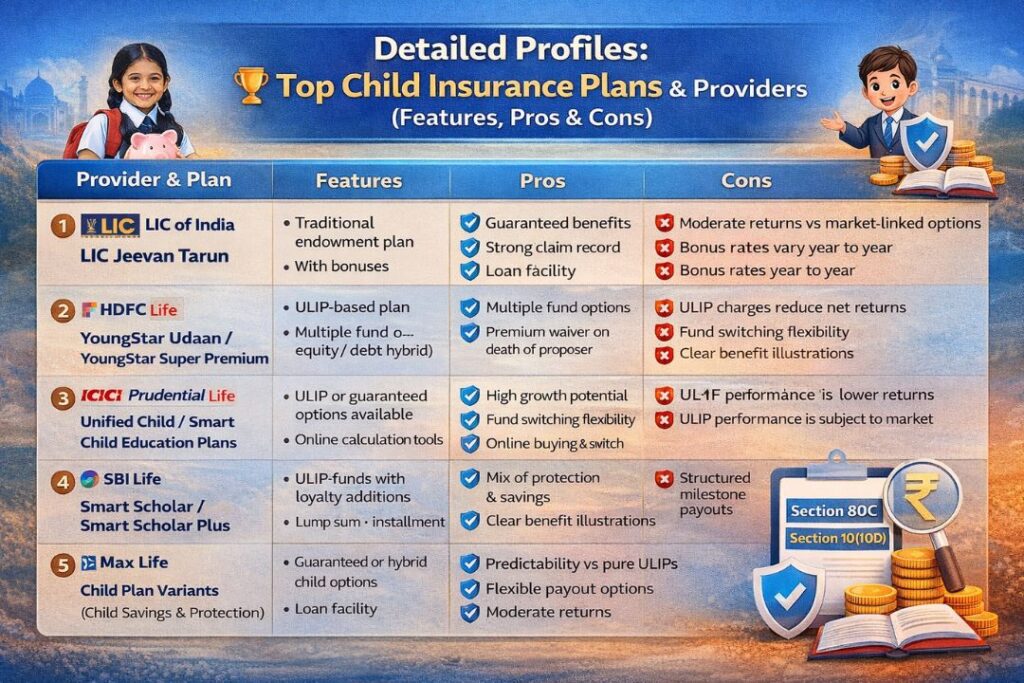

LIC of India—LIC child plans (example: Jeevan Tarun)

Overview & Suitability

LIC, as India’s largest public sector insurer, offers participating endowment-type child plans such as Jeevan Tarun and conventional children plans. These are classic guaranteed/participating plans targeted at conservative parents whose value guaranteed payouts and the security of a government-backed institution.

Key features commonly found in LIC child plans

- Entry age of child and proposal limits (e.g., child entry 0–12 yrs for some plans).

- Guaranteed sum insured with reversionary bonuses and final bonuses (if declared).

- Maturity benefits with bonuses sometimes staged payouts.

- Loan against policy after certain years.

- Premium waiver options under specific variants.

Who should buy

Conservative savers who priority guaranteed sums and want the LIC brand & branch network for servicing.

Watchouts

Returns are typically conservative.

Bonus rates depend on insurer’s surplus and can vary.

Compare real effective yields versus alternatives (term + mutual funds).

HDFC Life—YoungStar family: YoungStar Udaan, YoungStar Super Premium, Child Savings Plan

Overview & Suitability

HDFC Life offers a suite of child plans: ULIP-style market linked options (YoungStar Udaan, YoungStar Super Premium) and structured child saving. Their ULIPs are targeted at parents seeking market exposure with insurance benefits and flexible payout options.

Key Features

- Multiple fund options (equity, hybrid, debt)—you can choose fund allocation.

- Premium waiver on death of offeror (subject to terms).

- Guaranteed additions in certain variants, flexible payout options, and online purchasing convenience.

- Brochures and sales literature detail fund performance, allocation, and fees.

Who should buy

Parents convenient with equity exposure and looking for higher growth potential along with insurance cover and structured payouts.

Watchouts

- ULIP charges (allocation, fund management, mortality) can lower returns–check the fund fact sheet.

- Performance depends upon market returns; Select asset allocation based on risk profile.

ICICI Prudential — Unified Child/Child Education Plans

Overview & Suitability

ICICI Prudential offers both assured and ULIP-style child plans. Key selling points commonly include premium waiver options, staged payouts, and online purchasing.

Key Features

- Waiver of future premiums on assured event (death) so the corpus matures as intended.

- Guaranteed return plan varieties for risk-averse parents and market-linked ULIPs for growth seekers.

- Clear fund information and online tools to estimate premiums and maturity amounts.

Who should buy

Those who want a mix — reliable insurer with choices between guaranteed and market-linked variants.

Watchouts

- Compare net returns after costs. Read policy doc for survival / bonus schedules.

SBI Life – Smart Scholar and Smart Scholar Plus (ULIP education solutions)

Overview & Suitability

SBI Life’s Smart Scholar plans are unit-linked solutions created to build corpus for education with multiple fund options and loyalty additions. They often feature premium waiver and flexible payout structures (lump sum + instalments)

Key Features

- Market-linked growth through multiple fund options.

- Dual benefit of lump sum payout + premium waiver for policy continuance in an insured event.

- Loyalty additions and other ULIP features in certain variants.

Who should buy

Parents who want a large equities allocation potential with structured payouts for education.

Watchouts

- ULIPs need monitoring; Review fund performance annually and rebalance if necessary.

Max Life Insurance – child savings & protection options

Overview

Max Life offers child saving plans that typical combine guaranteed additions or market linkage with waiver of premium features and policy loan availability. Their focus is on flexible checkout options.

Who should buy

Parents wanting a balanced product with strong customer service and transparent disclosures.

Bajaj Allianz Life – child plans & differentiators

Overview

Bajaj Allianz offers ULIP and non-ULIP child solutions that stress flexibility and optional riders. They position some products with landmark payouts and premium waiver features.

Who should buy

Those looking for flexible plan features with personal insurer agility.

Tata AIA — child ULIPs/guaranteed alternatives

Source :Market aggregator listings.

Overview

Tata AIA’s child offerings frequently include ULIP options with fund choice and switching benefits; Some product versions include guaranteed extras or loyalty bonuses.

Exide Life Insurance – Guaranteed Options Under the Best Child Insurance Plans in India

Source: PolicyBazaar/Exide Life summaries.

Overview

Exide Life’s Mera Ashirwad (example) is a guaranteed child plan positioned for low-risk parents wanting secured landmark payouts.

Quick comparison notes & how to read product booklets

Official insurer pages and brochures list the UIN number, entitlement, exact payout schedule, premiums, fund details (for ULIPs), exclusions and terms. I used official product pages and brochures to collect the plan highlights above—please read the product brochure carefully (it’s the legally binding document).

Riders and waivers

Most child Insurance plans include or permit optional riders that significantly affect outcomes:

- Waiver of premium on death (most important): on the insured’s death, the insurer waives future premiums so the policy continues and the child still receives benefits. Confirm whether premium waiver is automatic or requires claim approval.

- Accidental death benefit rider: additional payout on accidental death of the assured. Good for additional protection but increases premium.

- Critical illness rider: Pays a sum upon diagnosis of defined critical illnesses; useful if the parent wants additional health protection.

- Hospital cash: less common in child plans, but available as an add-on in certain products.

Practical tip: the single most valued feature in a child plan is a reliable, clear premium-waiver clause that preserves the corpus in case the parent dies. If that clause has too many exclusions or long contestability periods, the plan’s protection value drops.

Taxation of the Best Child Insurance Plans in India – Basic Framework

Tax regulations are an important motivator for buying insurance. Broadly:

Premium deduction under Section 80C — Premiums paid for life insurance policies (subject to conditions and limits) can be claimed under Section 80C (limit currently ₹ 1.5 lakh per financial year). Check policy terms: For child policies where the proposer is the parent and premium is the parent’s, 80C normally applies subject to sum assured conditions.

Maturity proceeds under Section 10(10D) — maturity proceedings of life insurance policies are tax-exempt under Section 10(10D) if the policy meets prescribed conditions (e.g., sum assured thresholds and not classified as a money-saving instrument with taxability). ULIPs and conventional plans have had shifting tax treatments historically; Always confirm current tax rules with your tax adviser.

Note: Large bonuses, premium allocations, or payout structures can affect taxableness; tax rules change, so confirm at the time of purchase.

(Always consult a tax professional before relying on tax advantages.)

How to buy: practical checklist (documents, online versus offline)

Documents typically required

- KYC of proposer(PAN, Aadhaar, photo ID, address proof).

- Child’s birth certificate(proof of age).

- Proposal form duly signed.

- Bank mandate for auto-debit.

- Medical report (rare for lower sum assured but check if required for higher cover).

Online vs. Offline

- Online — faster, often lower commissions, instant illustrations, eKYC and eSign options. ULIPs and many child plans support online shopping.

- Offline/Agent – helpful for personalized advice The agent can explain riders and claim process. Make sure you get all documents and Free Look Period details.

Free Look Period

After purchasing, you usually have a free look period (15 days for online, 30 days for some offline) to review the policy and cancel for a refund if terms are dissatisfied. Use it to re-read the brochure and benefits illustration.

Claim, surrender, loan: practical examples and what to look for

Claim (death of proposer)

Example: Parent purchases a child plan with premium waiver on death. If parent dies, insurer must accept the claim (following documentation) and waive future premiums—the policy continues and child receives scheduled payouts. Check claim settlement process and turnover times.

Surrender

Early surrender frequently triggers low surrender value. Many plans only give significant returns if held to maturity. If you may need liquidity, choose products with flexible partial withdrawals or short lock-in restrictions.

Loan facility

Some plans allow loans against policy after a lock-in or surrender once value builds. Loan interest rates and limits vary read the policy.

Sample premium & maturity example (how to compare offers)

When comparing plans, always use the Guaranteed/Projected Benefit Example and compute:

- Total premiums paid(annual premium×term)

- Guaranteed maturity (if any)

- Projected maturity under reasonable return scenarios (For ULIPs, use 4%, 8%, 12% assumptions)

- Impact of charges (allocation, fund management, mortality) on returns

Example approach

- Pick a target corpus (e.g., ₹20 lakh when child turns 18).

- Use insurer calculators to find the premium for various plans under the same assumptions.

- Compare net returns and protection features (premium waiver) side by side.

Because calculators vary, save the insurer quotes (PDF) and compare table rows: Annual Premium | Total Premiums | Guaranteed maturity | Projected maturity at 8% | Waiver feature.

Final recommendations quick decision flow

If your priority is protection & low cost: buy an adequate term insurance cover (large sum assured for the parent’s life) and invest separately (mutual fund SIP/PPF) for the child’s future.

If your preference is guaranteed payouts & low risk: prefer a traditional participating child plan (e.g., conservative LIC/guaranteed variants).

If your priority is growth with landmark payouts: consider a ULIP child plan from a reputed private insurer (HDFC Life, SBI Life, ICICI Prudential) but keep an eye on charges.

Always insist on premium waiver on insured event—it’s the insurance value that preserves the corpus.

Conclusion

A child insurance plan is more than just an investment—it is a financial safety net that ensures your child’s dreams remain protected even in uncertain circumstances.

If you prefer:

- Security & stability – Choose traditional/guaranteed plans

- Growth potential – Select ULIP child plans

- Maximum cost-efficiency- Consider term insurance + mutual fund SIP strategy

Choosing from the Best Child Insurance Plans in India depends on how well the policy matches your financial goals, risk appetite, and long-term planning horizon.

Plan early. The sooner you start, the lower the premium and the higher the potential corpus.

Your child’s future deserves safe planning today.

Frequently Asked Questions

1.What is the ideal age to purchase a child insurance plan?

The earlier, the better. Purchasing when the child is 0–5 years old gives maximum investment horizon.

2.Is child insurance better than mutual funds?

Child insurance offers protection+savings. Mutual funds offer higher growth but no insurance coverage.

3.What happens if the parent dies?

Most plans:

- Pay immediate lump sum

- Waive future premiums

- Continue policy benefits

4.Can I withdraw money before maturity?

Yes, in Ulips after 5-year lock-in. Traditional plans may permit loans.

5.Are returns guaranteed?

Traditional and guaranteed plans offering assured returns. ULIP depends on market performance.

6.Is the maturity sum taxable?

Generally tax-free under Section 10(10D), subject to conditions.

7.Can I transfer funds in the Best Child Insurance Plans in India (ULIP Plans)?

Yes, most ULIPs permit fund switching.

8.What is premium waiver benefit?

This ensures that if the insured parent dies, future premiums are waived and the policy continues.

Disclaimer

This article on the Best Child Insurance Plans in India is for informational and educational purposes only. Insurance features, returns, tax rules, and policy conditions may change over time. Always read the official policy brochure, benefit illustration, and terms & conditions carefully before purchasing any insurance plan. Tax benefits are subject to prevailing laws. Please consult a licensed financial advisor or tax consultant before making any investment decisions.